FIRE Plan

When is it enough?

How bad do you need that stuff?

What’s it all for?

Why’s it seem like you still want more?

In the past few months, I’ve been thinking more about what my financial goals are and how I can attain them.

It’s mostly involved learning from other people but in this post, I want to explore what a roadmap to financial independence could look like.

Financial independence: When income from your investments alone is enough to cover all your expenses.

FIRE: Financial independence / retiring early

Now, there are plenty of shorter term goals, i.e. buying my first property, but I want to analyze what these goals entail separately so that by the end, I can:

- order them by my priorities,

- build a comprehensive, actionable financial plan for myself, and

- incrementally work towards them simultaneously

I’m starting with retirement because honestly, being 21 and graduating being the most pressing life goal in my short term future, it’s by far what I think about least.

I’m no expert so this for my own reference and perhaps food for thought.

Motivation

Goal: Afford retirement at 34, which gives me roughly 13 years from now. It seems ambitious but hey if I miss the goal, at least I’d still be on the right path.

I have no desire nor intention to retire at that age but if I can commit to the financial discipline, I could use the savings to instead seriously help support the retirement of my parents which is one of my personal goals.

If not, then use it for literally anything else ¯\_(ツ)_/¯

Retirement Math

This article outlines how long someone has to work before they’ve saved enough money to retire, where savings rate is the % of take-home pay (gross income after taxes) saved.

| Savings rate | Years until retirement is possible* |

|---|---|

| 0% | You will never retire |

| 10% | 51 |

| 30% | 28 |

| 40% | 22 |

| 50% | 17 |

| 60% | 13 ← where I want to aim to be |

| 80% | 6 |

| 100% | Working for fun! |

* Assuming 1) starting with a net worth of $0 and 2) earning 5% return on investment during saving years.

To afford retirement in 13 years, I need to save 60% (live on 40%) of my take-home pay. Sounds simple enough (at least in theory).

Expenses

From when I started university in 2017 til I promptly moved back home after COVID took over the world, I’ve lived in residence. When I’m not at res, I’ve lived at home. In short — I know nothing about what my real world expenses would look like.

But I can Google. And plan.

Budget Living in Toronto

These numbers are from a combination of real budgets from people on r/PersonalFinanceCanada and any expenses I have had. I’m going to err on the side of caution and make liberal estimates. Better over than under estimated in this case.

| Expense | Monthly Budget |

|---|---|

| Rent | $1,500 ← upper end of the $1-1.5K range w/ roommate |

| Groceries | $300 |

| Dining out | $200 |

| Phone | $60 |

| Internet | $70 |

| Subscriptions | $30 |

| Transit pass | $140 |

| Travel (Uber, etc) | $100 |

| Entertainment | $150 |

| Misc. | $450 ← whatever else |

| Total | $3,000/month |

In total, that’s $36,000/year of expenses. This obviously leaves a lot of room to save.

Let’s assume this lifestyle remains the same in retirement.

The Point of Financial Independence

Assuming a 4% safe withdraw rate (i.e. annual rate of return post inflation), I’d be able to cover those expenses yearly if I started with $36K / 4% = $900K.

This means if I had $900K saved a time of retirement, I can theoretically live off the interest earned off this at $36K yearly for the rest of my life.

The logic aka perpetuity:

Say I start the year with $900K. It earns 4% interest that year. By the end of the year, that money has grown to 900K * 1.04 = *$936K. I withdraw the $36K to live on, leaving me with $900K. Rinse and repeat the next year, effectively infinitely earning $36K a year.

Income

Based on the chart above, to be retirement ready in 13 years, I need to be living on 40% of my income. For 17 years, 50%.

To hit those target percentages, I can focus this effort on increasing savings or increasing income. Ideally, I want to optimize both. But for now, let’s assume I don’t want to compromise this lifestyle; how much do I need to make to sustain $36K yearly?

Income Needed for $36K Yearly Expenses at Different Rates

Spending rate = % of take-home pay I’m living on = 100% - savings rate.

So if $36K expenses is spending 40% of my take-home, I need $36K / 0.4 = $90K.

| Spending rate | Take-home needed | Approx. pre-tax income (Ontario) |

|---|---|---|

| 60% | $60K | $81K |

| 50% | $72K | $100K |

| 40% | $90K | $130K |

Side note: as an example of the effects of increasing savings, let’s say I saved an extra $500 a month for a total yearly expense of $30K. For this to represent a 40% spending rate, I’d need a take-home of $75K, meaning saving that extra $6K results in $15K less income need to hit the same target retirement year.

Understanding Compound Interest

Okay, so if I save X% of my income, what does it actually look like year to year.

These scenarios correspond with the table above:

- Saving 40% of take-home of 60K = saving $24K/year

- 50% of 72K = $36K/year

- 60% of 90K = $54K/year

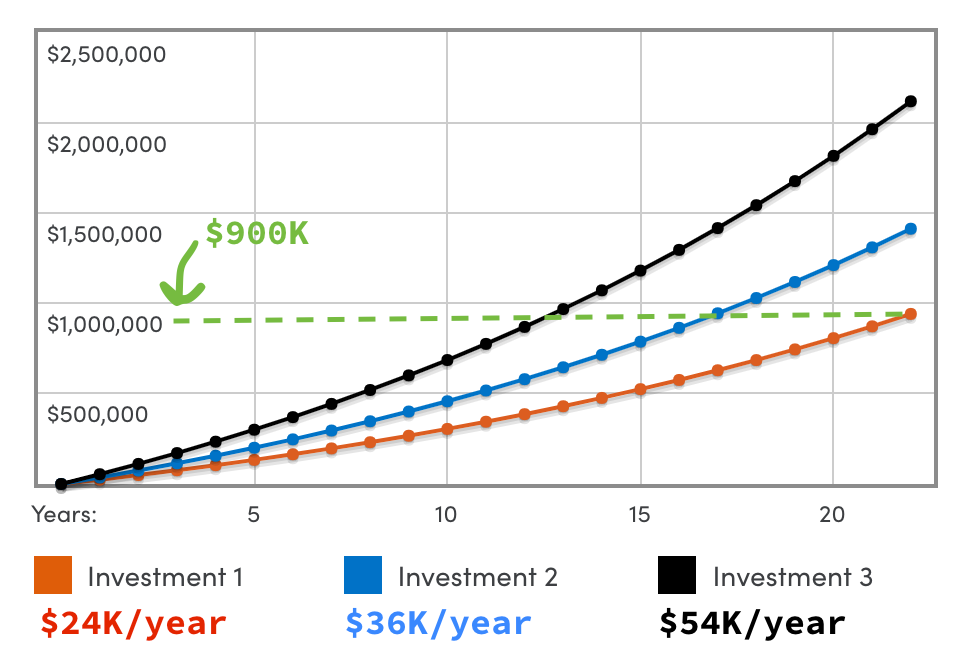

Using this online calculator, what my investments could look like before tax.

Assuming 5% return compounded annually with a starting balance of $0.

Assuming 5% return compounded annually with a starting balance of $0.

The investments pass the target threshold of $900K at 22 years ($24K/year), 17 years ($36K/year), and 13 years ($54K/year).

Beyond the % or amount of savings, there’s another factor to consider: time. That’s when the power of compound interest really starts to shine.

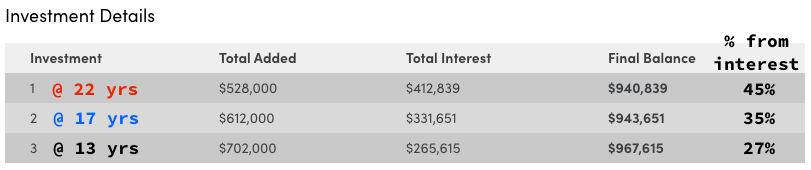

Snapshot of investments around the year they pass the $900K threshold

Snapshot of investments around the year they pass the $900K threshold

Obviously these calculations are very rough but by adding 4 years to my timeline — from 13 to 17 years — compound interest would do approx. 8% more of the work for me, saving me tens of thousands in out of pocket contributions.

Much to think about.

Before I started really thinking about finance, these numbers and goals seemed far and beyond reach; power comes with demystifying the math and making a plan that I eventually want to turn into an automated savings system. A few back of the envelope calculations later and I’m much better off than when I began.

Of course, there are a lot of variables at play in real life and money, or even financial independence, is not something I ever want to compromise a fulfilling life. I often find myself contemplating the value in chasing money beyond the point of covering my needs and reasonable wants but the answer I’ve settled on is that it can afford a sense of freedom that I want to provide my family, myself, and hopefully others.

Cool cool, now time to shift focus to software developer new grad offers.

Some Resources That Inspire Me

Here are some sources of real life experiences I enjoy keeping up with:

- Sosa on YouTube — a black woman in software engineering!!! How I Bought My First Rental Property at 23 is basically where I want to be

- Millennial Money series on YouTube — this episode features another black woman software engineer!!

- Graham Stephan on YouTube

- r/PersonalFinanceCanada on Reddit